DELTA EXCHANGE WHITEPAPER

Executive Summary

About Delta Exchange |

Delta Exchange is a cryptocurrency derivatives exchange. We have been operational since August 2018. Our investors include AAVE ventures, Kyber Network,CoinFund, QCP Setoria, Spartan Group, Sino Global, Gumi CC, BR Capital, Tomo Chain, LuneX Ventures, g1 Capital etc. |

Current status |

|

DETO |

|

DETO Tokenomics |

|

Delta Exchange

About the Exchange

Delta Exchange is a cryptocurrency derivatives exchange that offers trading in a wide variety of derivative contracts. We list perpetual swaps on over 90 cryptocurrencies/ crypto-assets and options on BTC and top altcoins such as ETH, LTC, BCH, BNB and LINK. Additionally, we offer a variety of innovative products that are unique to us. These include Turbo options (knock-out options), MOVE (straddles), calendar spreads and interest rate swaps.

Our vision is to build the world’s most liquid, advanced and recognized cryptocurrency derivatives exchange for retail and institutional market participants. Most existing crypto exchanges are lacking in some or all of the four key dimensions: liquidity, reliability, fairness, and transparency. We strive to achieve excellence across all these dimensions.

Our success is inextricably tied with the success of our customers. Thus, providing a fair and trustworthy trading venue is not only the right thing to do, but is also a savvy business strategy. Even though we are self-regulated, we are committed to providing democratized access to a multitude of cryptocurrency derivative products to traders globally.

Salient Features

Proven track record

We have been operational since August 2018. Within three years, we have been able to build a world-class exchange that is at par or ahead of the competition. In the 3+ years that we have been operating, we have traversed a steep learning curve and earned insights into customer behaviour, market dynamics and the key challenges in running an exchange.

The A-team of crypto

We understand derivatives, have the know-how of creating new financial products and have the experience of building products that scale to millions of users. Two of the three founders of Delta Exchange come from blue-chip Wall Street firms (Citi, UBS, GIC). The third founder is a serial entrepreneur with significant experience in building scalable systems. While we come from different backgrounds, we are united in our passion for crypto.

Battle-tested trading systems

We have already written our trading systems from scratch twice. They have performed well under demanding conditions during heightened volatility. Keeping scalability in mind, we have chosen Elixir (a variant of Erlang) for our stack. Our matching engine can handle 1mn transactions per second and our API gateway is currently handling 200K requests per min and is scalable to 5mn requests per min. The matching engine and other systems are implemented with sharding across contracts to provide great horizontal scalability.

Demonstrated ability to innovate

We have consistently launched new features and unique derivative products, displaying our ability for original thinking. We were the first exchange to offer stablecoin settled futures. Likewise, we pioneered altcoin futures. Interest rate swaps, Calendar spreads and Turbo Options are one-of-a-kind products with which we have pushed the envelope for crypto derivatives.

Current State of Things

Daily trading volumes | ~$900mn |

Registered users | 216,500+ |

Product portfolio |

|

Key features |

|

Listings and integrations |

|

Community |

|

What will Help us Win

Crypto derivatives are rapidly growing and a hotly contested space. Although for us, meaningful competition comes from a handful of firms only, some of our competitors are much bigger and much better capitalised than us. We believe that we are capable of stealing a march on competition and becoming the go-to crypto derivatives exchange.

Pioneer crypto options

Crypto options trading is on the cusp of explosive growth. Currently, Deribit is the dominant player in crypto options. However, 80% of their options trading volume is institutional. If you look at equity markets, options trading tends to have large retail participation. There is no reason for crypto options to be any different. Retail and professional traders will likely drive the next leg of growth in crypto options trading. We believe our options offerings resonate with retail investors because:

- our contracts are vanilla and not inverse

- we have smaller contract size that are suitable for retail traders,

- our UI is intuitive and easy to use

- all our options contracts are margined and settled in USDT. This is different from other exchange where the margining and the underlying currency are the same, for e.g., BTC options are margined in BTC and ETH options are margined in ETH.

- we are the only exchange to have options on top altcoins such as BNB, LINK, Solana, Matic, LTC and XRP.

We have successfully attracted retail traders and taken away market share from the competition in the options market.

Launch innovative products to acquire customers

Innovative products help us acquire new customers. Customers who sign up for new and unique products, end up trading standard products such as bitcoin perpetuals as well. In our 3+ years of operations, we have launched several innovative products such as interest rate swaps and Turbo options. These products help us differentiate from competitors and grow by expanding the market. Innovation will remain a key aspect of our growth strategy.

Focus on customers, not competition

We are laser focused on giving our customers the best possible trading experience. While deep liquidity, high availability and safety of crypto in custody are key, there are other aspects of trading business that seem peripheral but are important to customers. These include support and ancillary tools (e.g., tax calculator and portfolio analytics). We continue to focus on these areas. We aspire to emulate Amazon and be the most customer-centric company in the cryptocurrency domain.

Revenue Model

When two parties trade on Delta Exchange, we earn taker and maker fees. All the derivative contracts listed on the exchange and margined and settled in either BTC or USDT. Consequently, we earn all our revenues in BTC or USDT. Our current trading fees schedule is as follows:

Contract Category | Taker Fee | Maker Fee |

Futures: inverse contracts | 0.05% | 0.02% |

Futures: USDT settled linear contracts | 0.05% | 0.02% |

Futures: Alt-BTC contracts | 0.10% | 0.10% |

Commodity futures | 0.15% | 0.15% |

Options | 0.03% | 0.03% |

Calendar spreads | 0.05% | 0.05% |

Interest rate swaps | 0.10% | 0.10% |

Delta Exchange Token (DETO)

What is DETO

DETO is an ERC-20 utility and rewards token that will become an integral part of Delta Exchange. Through DETO, we plan to create incentives for active traders and liquidity providers to participate in and contribute to the Delta Exchange ecosystem. And, the tokenomics of DETO are such that its value is directly linked to the growth of the exchange. These dynamics will result in a virtuous growth loop. The DETO driven incentives will lead to greater liquidity and trading volumes at the exchange. This in turn will increase the value of DETO based rewards, creating an even stronger pull to participate in the Delta Exchange ecosystem.

DETO Utility

The functionalities that DETO will have on Delta Exchange are listed below. These have been carefully designed to increase the demand of DETO and reduce its circulating supply and thus, will give a boost to the value of DETO.

Trading fee payment method

Customers will have an option to pay 25% of their trading fees in DETO. Delta Exchange will accept this DETO at a price which is higher of: market price of DETO at that time and the Minimum Support Price (MSP). Currently, MSP has been set at $1.

MSP should serve as a floor on the market price of DETO. Market prices going below the MSP will create arbitrage-like opportunities for traders on Delta Exchange. They will be able to buy DETO below MSP and immediately realise a higher price (MSP) by using the DETO to pay trading fees.

Collateral

DETO will be allowed to be used as margin for trading on Delta Exchange. This feature will be enabled once we launch multi-asset collateral. Thus traders will be able to margin positions in DETO, even though the settlement will happen in BTC or USDT.

There are several advantages to using DETO to collateralise open positions: (a) demand for DETO will increase as trading activity and open interest on the exchange grows, and (b) margined DETO will be effectively locked up, thus reducing the circulating supply.

DETO margined & settled financial products

We plan to launch structured products (e.g., exotic options, income-generating products) that will be margined and settled exclusively in DETO. In traditional finance, such products enjoy significant popularity, and we believe that the same success can be achieved in crypto.

DETO denominated insurance fund

Delta Exchange currently has an insurance fund composed of BTC and USDT denominated pools. We plan to launch a DETO denominated pool to supplement that existing insurance funds. DETO holders will be able to stake DETO into the pool and earn yield.

In the rare situations when the system ends up closing some positions with negative equity, the DETO in the pool may be drawn down to ensure full payout to the winning traders. We will aim to maintain the staking yield at a level where the returns (from staking & potential DETO price appreciation) should more than offset the risks of drawdown from the pool.

We believe that this innovative staking program will kill two birds with one stone:

(a) reduce the circulating supply of DETO and

(b) help us create a large insurance fund, which in turn should help us attract large trading firms and funds to trade on Delta Exchange.

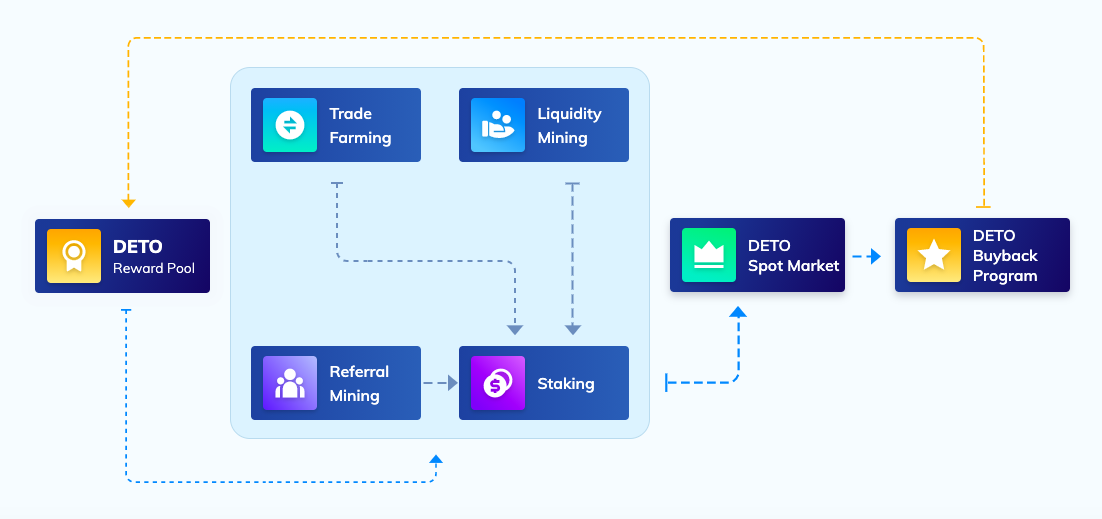

DETO Rewards Program

DETO is intended to be much more than a utility token. We plan to create an expansive yet sustainable rewards program centered around DETO. The overarching goal of the rewards program is to incentivize traders to participate in trading and other aspects of Delta Exchange. We would reward DETO to active participants in the Delta ecosystem. DETO based incentives will help us acquire more traders and provide an impetus to trading volumes.

We have committed 100 million DETO (20% of the token supply) to the rewards pool. We plan to distribute these tokens roughly over a 12-18 month period. This means about 200,000 DETO will be given as rewards daily for participating in farming, mining or staking on Delta Exchange. It is worth noting that we may change the DETO reward allocation to specific activities, introduce DETO rewards for new activities and increase/ decrease the daily rewards based on market conditions and business requirements. However, we will aim to stay close to our target of giving 100 million DETO in the first 12-18 months after the token launch.

Liquidity Mining (Robo-trading & AMM Pools)

Delta Exchange has a robo-trading marketplace, where users can deploy capital into a wide variety of algorithmic trading strategies such as AMMs (automated market makers) and trend-following algos. Customers will earn DETO from the daily liquidity mining rewards pool, in proportion to their share of capital deployed in the trading strategies pools.

Trade Farming

Traders on Delta will earn DETO from the daily trade farming rewards pool, in proportion to their share of trading on Delta Exchange. All active traders on Delta Exchange will automatically be eligible for trade farming rewards.

Referral Mining

Customers or professional affiliates will earn DETO on the trading activity of their referred users. The daily DETO referral mining reward pool will be distributed among all the referrers in proportion to the trading volumes done by their referred users.

Staking

As described above, the staking program will primarily be used to set up a DETO denominated insurance pool. Additionally, we will opportunistically launch (risk-free) deposit schemes aimed at reducing circulating supply of DETO. Obviously, the staking yield in the DETO insurance pool will be higher than that in those deposit schemes.

Modus operandi of the rewards program

At any given time, we might be running multiple incentive schemes with DETO rewards. All these schemes will broadly follow the same rewards structure.

- A scheme will have a pre-specified daily reward pool. DETO in the pool will be distributed between the participants in proportion to their contribution.

- The daily reward pool will not scale up/ down with the number of participants/ level of activity. Only the distribution of the same reward pool will change. For example, trade farming rewards will not increase proportionally with trading volumes. This structure disincentivizes unscrupulous behaviour (e.g., wash trading) to earn rewards.

- All DETO earned as rewards will be subject to a vesting schedule.

Sustaining the rewards program

Several projects in both CeFi and DeFi have successfully leveraged incentive schemes such as trade farming and liquidity mining to overcome the bootstrapping problem and achieve quick growth. However, in many cases, activity levels peter out once the reward taps are turned off.

We aspire to create a large and enduring business and hence sustainable growth is what we are after. With this in mind, we have carefully designed our rewards program to provide a strong but steady fillip to our trading volumes, for years to come.

To sustain the DETO based incentive programs, we would need to keep topping up the rewards pool. The 100 mn DETO allocated to the reward pool should last for 12-18 months. Subsequently, the reward pool will be replenished with: (a) DETO acquired through the buyback program (described in the next section) and (b) freshly minted DETO (details are provided in the section on supply schedule).

This closing of the loop with the DETO buyback program will enable us to sustain the rewards program for as long as it yields a positive ROI. It is important to note that as the crypto derivatives landscape evolves, change in customer profile or competitive dynamics may warrant a different type of incentive program. Therefore, our rewards programs will continue to evolve too, even though the foundational philosophy of using DETO based incentives to fuel growth will remain unchanged.

DETO Buyback Program

25% of the trading fees that Delta Exchange earns will be used to buy freely circulating DETO, with the aim of reducing circulating supply. The DETO buyback program will begin from June 2021 and will continue at least until 50% of the supply hard cap (i.e., 375mn DETO) have been bought back. For the sake of clarity, the DETO that is used to pay trading fees will be considered as part of the buyback program.

Bought back DETO. Now what?

Let’s look at the world of equities. A company can either reinvest its income or use it for cash distributions (dividends, share buybacks). A company that is in growth mode reinvests to increase its revenues and profits. In contrast, a mature company, with limited opportunities to grow, tends to favour cash distribution.

We face similar choices for the bought back DETO. We can plough it back in the business to fuel growth of trading volumes and revenues. Or, we could take the well beaten path of burning the bought back tokens. Which choice has the higher ROI?

Given the state of maturity of crypto derivatives trading and our current scale, we believe that chasing growth makes the most economic sense. Therefore, our current plan is to funnel the bought back DETO to the rewards pool for as long as it makes sense. That said, periods of strong growth may be punctuated by sluggish markets. During these lulls, burning the bought back tokens might yield better returns.

Taking a long term view of things, and factoring in the uncertainties, we have decided to keep the discretion of choosing between growth and burn with the management of Delta Exchange.

The Virtuous Growth Loop

We now have the full picture to see the virtuous growth loop we are aiming to create by leveraging DETO. DETO based incentive schemes will help us to attract more traders and other contributors, leading to increase in trading volumes and revenues. More revenues mean great ability to buy back DETO, which will be used to replenish the rewards pool. At the end of each cycle, we should end up with higher trading volumes, higher trading fee revenues and higher value of DETO.

DETO Tokenomics & Metrics

DETO is an ERC20 token. At the Token Generation Event (TGE), 500mn DETO will be minted. DETO supply is hard capped at 750mn. In the 18 months following the TGE, no new tokens can be minted. After that a maximum of 25mn tokens can be minted in any quarter. In the limiting case, when 25mn tokens are minted every quarter starting with Q7, the token supply hard cap would be reached in 4 years from the TGE. Newly minted tokens will be allocated to the rewards pool and the treasury.

It is worth noting that the 25mn is the upper limit on the number of tokens that can be minted in a quarter. Depending on the market conditions, a company can choose not to mint in a given quarter. This has two implications: (a) 4 years is the earliest possible time for reaching supply hard cap. Actual time needed to reach there may be longer and (b) we may never reach the supply hard cap, if the company decides against minting new tokens.

Token emission schedule (assuming minting in consecutive quarters after the first 18 months)

Token allocation

At TGE | At time when supply = hard cap | |||

Tokens (mn) | % Share | Tokens (mn) | % Share | |

Treasury | 83.7 | 16.7% | 208.7 | 27.8% |

Reward Pool | 100.0 | 20.0% | 225.0 | 30.0% |

Equity holders | 175.0 | 35.0% | 175.0 | 23.3% |

Private Sale | 103.8 | 20.8% | 103.8 | 13.8% |

Employees & Advisors | 37.5 | 7.5% | 37.5 | 5.0% |

Total | 500.0 | 100.0% | 750.0 | 100.0% |

Vesting schedule

Category | % vested at TGE | Wait Period | Vesting Period |

Reward pool | 0% | 0 | 12 months |

Private sale investors | 0% | 1-3 months | 6 months |

Equity holders | 0% | 12 months | 12 months |

Team & Advisors | 0% | 6 months | 6 months |

Treasury | 20% | 1 month | 12 months |

Founders | 0% | 12 months | 24 months |

* Equity holders do not include founders here

** No vesting happens during the wait period

*** Daily equal number of tokens are vested over the vesting period. For example, if 90 tokens are to be vested over 3 months, every 90/ (3*30) = 1 token would be vested

Token Circulating Supply Schedule

Roadmap

1Q-2022 |

|

2Q-2022 |

|

3Q-2022 |

|

Team

Founders

The team has the right mix of finance and tech expertise and has previously worked with Wall Street firms as traders and research analysts and have built VC funded tech startups with millions of users.

Pankaj Balani (Chief Executive Officer | LinkedIn Profile | Twitter)

Pankaj has spent over 6 years in derivatives trading in Hong Kong and India at wall street giants such as UBS. He has deep experience in derivatives, quantitative finance and Asian equity markets. Pankaj also helped build and grow an e-commerce business in India which went on to raise Series C round of financing.

Jitender Tokas (Chief Business Officer | LinkedIn Profile | Twitter)

Jitender has worked with Citigroup in India and GIC in Singapore. In his 8+ years career in financial services, Jitender has been both an institutional investor and equity research analyst and helped two Indian Internet companies raise money from public markets.

Saurabh Goyal (Chief Technology Officer | LinkedIn Profile | Twitter)

Saurabh is a serial entrepreneur and a seasoned tech leader. He first co-founded Housing.com which went on to raise money from Softbank. Saurabh then built and sold a FoodTech company, TinyOwl that scaled to 1.5mn users, 1200 employees and raised USD ~25mn from the likes of Sequoia, Matrix and Nexus. Saurabh was also the Director of Engineering at Hostar — a video streaming platform which has over 20mn users and handles ~5mn concurrent users.

Advisors

The founding team is ably mentored and supported by a group of current and ex entrepreneurs, leading academics and Wall Street veterans.

Prof Bhagwan Chowdhry (LinkedIn | Twitter)

Prof. Bhagwan Chowdhry is currently a Professor of Finance at Indian School of Business; one of the premier business schools of India. He was also a Research Professor at UCLA Anderson School of Management. Prof Chowdhry advises a number of fintech companies including Stellar Development Foundation. He has also taught at the University of Chicago, University of Illinois at Chicago and the Hong Kong University of Science and Technology and has served on the editorial boards of several finance and economic journals.

Bernard van Bunnik (LinkedIn)

Bernard van Bunnik is currently the CEO and Chairman of Du Bois Gold. He has also been a Chairman-director and impact investor in multiple Fintech and Mobility start-ups; and also an advisor to PE and VC funds. Bernard's corporate work experience spans across being the CEO, Chairman and NED in 6 countries for 19 years working with GE Capital across Asia, AU-NZ, UK, Europe, US. He has also worked at McKinsey and Company in 4 countries for 5 years.

Jitendra Gupta (LinkedIn |Twitter)

Jitendra is currently the Founder & CEO of Jupiter, India's first digital-only bank. Previously, Jitendra founded Citrus Pay which he successfully grew to a 300+ strong team and raised over USD 30Mn. Citrus was acquired by PayU; where he served as the Managing Director.

Dan Clarke (LinkedIn, Twitter)

Dan was the CMO of Taiwan’s largest digital asset exchange, MAX Exchange. Prior to this, he was the Taiwan country head for both Barclays and Macquarie. A seasoned Wall Street veteran whose career spans 20 years across various financial markets, working with prominent investment banks across Asia and Europe.

Legal Disclaimer

PLEASE READ THIS DISCLAIMER SECTION CAREFULLY.

General information

The Delta Exchange Tokens (DETO) (“Tokens”) are intended to be issued by DOTE Labs Ltd with registered offices at CCP Financial Consultants Limited, Ellen L. Skelton Building, Fishers Lane, Road Town, Tortola, British Virgin Islands (“Issuer”) and which are to be generated by and recorded on a blockchain network supported by a smart contract software application developed/executed by the Issuer.

The Tokens are designed as a hybrid token (cryptocurrency and utility) and therefore, according to their structure, are not legally considered as a security or share since it does not give rights to dividends, interest, profit-sharing, or any other remuneration related to Issuer and do not represent any claim for repayment of a monetary sum against the Issuer. Persons holding Tokens do not have any claim against the Issuer for payment of interests or for sharing of profits generated by the Issuer.

The Tokens will be tradeable on and may be accepted for derivative transactions and/or other services on the Delta Exchange but do not have any value, rights, uses, purposes, attributes, functionalities or features, express or implied, outside of the Delta Exchange. Delta Exchange is owned and operated by BitProtocol Ltd. incorporated in Saint Vincent and the Grenadines with its registered address at Euro-Caribbean Trustees Limited, First Floor, First St Vincent Bank Ltd Building, James Street, Kingstown, St Vincent and the Grenadines (“Delta Exchange”). Delta Exchange is an affiliate of the Issuer and the Issuer, Delta Exchange and/or their respective affiliates shall hereinafter be collectively referred to as “Issuer Parties”).

A total loss of the value of Tokens or any investment due to various causes cannot be excluded. Accordingly, they cannot and should not be purchased for speculative or investment purposes.

No person should purchase tokens unless he/it has the necessary knowledge and expertise, understands the characteristics of the Tokens, and has read and fully understood and accepted the risks outlined in this Whitepaper.

THIS WHITE PAPER IS FOR PROJECT DESCRIPTION AND INFORMATIONAL, ILLUSTRATION AND DISCUSSION PURPOSES ONLY AND DOES NOT IN ANY WAY CONSTITUTE A PROSPECTUS OR OFFERING DOCUMENT. IT IS NOT INTENDED TO CONSTITUTE AN OFFER TO SELL, OR AN INVITATION TO AN OFFER TO BUY AND/OR SUBSCRIBE.

THIS WHITEPAPER IS ALSO NOT INTENDED AS A SOLICITATION TO INVEST IN SECURITIES OR ANY OTHER FORM OF INVESTMENT PRODUCTS. THIS WHITEPAPER, IN WHOLE OR IN PART, AND THE COPY THEREOF, MUST NOT BE TAKEN OR TRANSMITTED TO ANY COUNTRY WHERE THE DISTRIBUTION AND DISTRIBUTION OF WHITEPAPERS IS PROHIBITED OR RESTRICTED.

THIS WHITE PAPER DOES NOT CONSTITUTE INVESTMENT, ECONOMIC, LEGAL, TAX, REGULATORY, FINANCIAL, ACCOUNTING OR OTHER ADVICE, AND IS NOT INTENDED TO PROVIDE THE SOLE BASIS FOR ANY EVALUATION OF A TRANSACTION ON ACQUISITION OF TOKENS.

No legal effect

This White Paper does not give rise to any binding contractual relationship. The content of this White Paper is not binding for the Issuer and is subject to change in line with the ongoing research and development of the Delta Exchange. No legal relationship is established between a purchaser of the Tokens and the Issuer unless the Issuer enters into separate individual legally binding agreements and/or terms and conditions with such purchaser, and the rights and obligations of a token purchaser and the Issuer shall be subject only to such aforementioned separate individual legally binding agreements and/or terms and conditions.

No representation or warranty

The information contained in this White Paper is for general understanding purposes and presentation purposes only. The Issuer does not represent or warrant or provide any guarantee, promise or commitment on the objectives, performance or results anticipated to be achieved as set out in this White Paper.

The Issuer endeavours to keep the information contained in this White Paper up-to-date and correct, however, the Issuer has no obligation to update or keep current any information or projections contained in this White Paper. The Issuer does not make any representation or warranty of any kind as to the accuracy, completeness, reliability, suitability or availability of the information contained and the conclusions reached in this White Paper.

Calculations, forecasts and forward-looking statements

The information set forth in this White Paper may not be exhaustive. The calculations and forecasts in this White Paper are essentially based on the experiences or assessments of the management of the Issuer. In this respect, this White Paper contains forward-looking statements, in particular subjective objectives of the future business development, which are associated with uncertainties and risks.

Opinions, assumptions, assessments, (forward-looking) statements or the like reflect the current state of perceptions and expectations of the Issuer and constitute only subjective views, beliefs, outlooks, estimations or intentions of the Issuer. These perceptions and expectations may contain perception errors and errors of assessment and thus prove to be incorrect. The calculations were made with care and with commercial caution. Nevertheless, it cannot be excluded that events or developments, which were not taken into account within the calculations and forecasts, lead to significant deviations of the and/or possibly to a deterioration in the value of the Tokens.

Opinions, assumptions, assessments, (forward-looking) statements or the like should not be relied on, are subject to change due to a variety of factors, including fluctuating market conditions and economic factors, and involve inherent risks and uncertainties, both general and specific, many of which cannot be predicted or quantified and are beyond the control of the Issuer. Therefore, there can be no assurance that the events and developments described in this White Paper can be achieved. The token purchaser bears the risk of deviating events and developments.

Risk Factors

- Risk of total loss. Tokens may have no value and Purchaser may lose all amounts paid.

- No Rights, Functionality or Features. Tokens have no rights, uses, purpose, attributes, functionalities or features, express or implied and they do not necessarily have any use or value.

- Internet Transmission Risks. There are risks associated with using Tokens including, but not limited to, the failure of hardware, software, and internet connections. Transactions in cryptocurrencies may be irreversible, and, accordingly, losses due to fraudulent or accidental transactions may not be recoverable. Cryptocurrency transactions are deemed to be made when recorded on a public ledger, which is not necessarily the date or time when the transaction is initiated.

- Malfunctions, bugs and weaknesses. There is a risk that the token smart contract may contain intentional or unintentional bugs or weaknesses or suffer malfunctions which may negatively affect Tokens or result in the loss or theft of Tokens or the loss of ability to access or control Tokens. In the event of such a software bug or weakness, there may be no remedy and Token holders are not guaranteed any remedy, refund or compensation.

- Dependence on Management Team. The ability of each of the Issuer Parties’ management and project teams, which are respectively responsible for maintaining the competitive position of the Tokens and Delta Exchange, is dependent to a large degree on the services of their management teams. The loss or diminution in the services of members of such senior management team or an inability to attract, retain and maintain additional senior management personnel could have a material adverse effect on the Tokens and the Delta Exchange. Competition for personnel with relevant expertise is intense due to the small number of qualified individuals, and this competition may seriously affect such entity's ability to retain its existing senior management and attract additional qualified senior management personnel, which could have a significant adverse impact on the Tokens and the Delta Exchange.

- No Rights, Functionality or Features. It is possible that the Tokens will not be used by a large number of individuals, businesses and organizations and that there will be limited public interest in the creation and development of its functionalities and lack of commercial success or prospects. Such a lack of interest could impact the development of the Tokens.

- Risks related to Reliance on Third Parties. The Token smart contract and Delta Exchange will rely, in whole or partly, on third-parties to adopt and implement it and to continue to develop, supply, and otherwise support it. There is no assurance or guarantee that those third-parties will complete their work, properly carry out their obligations, or otherwise meet anyone’s needs, any of which might have a material adverse effect on the Tokens.

- Changes to functionalities and features of Tokens. The functionality and features of the Tokens are still under development and may undergo significant changes over time. Although Issuer intends for the Tokens to have the features and specifications set forth in the White Paper, changes to such features and specifications may be made for any number of reasons, any of which may mean that the Tokens may not meet expectations of the Purchaser.

- Risks related to Reliance on Third Parties. The Token smart contract and Delta Exchange will rely, in whole or partly, on third-parties to adopt and implement it and to continue to develop, supply, and otherwise support it. There is no assurance or guarantee that those third-parties will complete their work, properly carry out their obligations, or otherwise meet anyone’s needs, any of which might have a material adverse effect on the Tokens.

- Changes to functionalities and features of Tokens. The functionality and features of the Tokens are still under development and may undergo significant changes over time. Although Issuer intends for the Tokens to have the features and specifications set forth in the White Paper, changes to such features and specifications may be made for any number of reasons, any of which may mean that the Tokens may not meet expectations of the purchaser.

- Other Projects. The token smart contract and Tokens may give rise to other, alternative projects, promoted by parties that are affiliated or unaffiliated with the Issuer Parties, and such projects may provide no benefit to the Tokens or Delta Exchange.

- Liquidity Risks. Tokens may have no value, and there is no guarantee or representation of liquidity for the Tokens and/or the availability of any market for Tokens through third parties or otherwise.

- Token Security. Tokens may be subject to expropriation and or/theft and holders of Tokens are not guaranteed any remedy, refund or compensation. Tokens purchased may be held in a purchaser’s digital wallet or vault, which requires a private key, or a combination of private keys, for access. Accordingly, loss of requisite private key(s) associated with a purchaser’s digital wallet or vault storing Tokens will result in loss of such Tokens. Moreover, any third party that gains access to such private key(s) may be able to misappropriate Tokens.

- Non-Transferability. Vesting and/or lock-up periods may apply, during which the Tokens may not be transferable.

- New Technology. The smart token contract, the Tokens and all of the matters set forth in the White Paper are new and untested and might not function as intended.

- Uncertain Regulatory Framework. The regulatory status of cryptographic tokens, digital assets and block chain technology is unclear or unsettled in many jurisdictions and is subject to significant uncertainty. It is difficult to predict how or whether governmental authorities will regulate such technologies. It is likewise difficult to predict how or whether any governmental authority may make changes to existing laws, regulations and/or rules that will affect cryptographic tokens, digital assets, block chain technology and its applications. Such changes could negatively impact Tokens in various ways, including, for example, through a determination that Tokens are regulated financial instruments that require registration. Issuer may cease the distribution of Tokens, or cease operations in a jurisdiction in the event that governmental actions make it unlawful or commercially undesirable to continue to do so.

- Risks Arising from Lack of Governance Rights. As Tokens confer no governance rights of any kind with respect to the Delta Exchange or the Issuer Parties, all decisions involving the services available on the Delta Exchange, features and functionalities of the Tokens or relating to any of the Issuer Parties will be made by the Issuer Parties at their sole discretion, including, but not limited to, decisions to discontinue services or Tokens, to create and sell more Tokens, or to sell or liquidate the Issuer. These decisions could adversely affect the Delta Exchange and the utility of any Tokens, including their utility for obtaining services.

- Tax Risks. The tax characterization of cryptographic tokens is under development in different jurisdictions and it is possible that adverse tax consequences, including withholding taxes, income taxes and tax reporting requirements may result from purchasing or holding Tokens

- Operative and Financing risks. The Issuer is a start-up and has a short operating history, limited profits and cashflow. There may be difficulties, complications and delays in developing a new business model and other issues frequently encountered in connection with new or developing businesses, including uncertain market acceptance, competition and lack of revenue. Its operations depend on generating adequate funding for the development and expansion of the business (including the maintenance of an infrastructure for using the Token). Should the Issuer not be successful in generating adequate funding, there is a risk that the Issuer cannot develop and expand its business operations as planned and may wholly or partly cease its business operations or become insolvent. Such a development could have a lasting negative effect on the usability or intrinsic value of the Tokens.

- Unanticipated Risks. Cryptographic tokens are a new and untested technology. In addition to the risks discussed above, there are risks that we cannot anticipate. Further risks may materialize as unanticipated combinations or variations of the discussed risks or the emergence of new risks.