How Delta’s AMM Pools Work – Democratizing Market Making

Overview of Delta's AMM Pools

Our overarching goal behind launching AMM Pools is to democratize market making. In TradFi, market making has been the dominion of a handful of specialized firms. These firms develop proprietary trading strategies and typically use their own capital to make markets and generate an attractive stream of largely uncorrelated returns. A typical retail investor does not have:

- Capability to develop robust trading strategies.

- Maintain the IT infra required to run highly latency sensitive market making strategies.

- Sufficient capital to be able to become an effective market maker.

Moreover, considering market making firms typically work with their own equity or debt, even large investors have limited access to the alpha from market making. Our AMM pools will solve for these constraints and make investing in a market making strategy accessible to everyone. We achieve this by:

- aggregating capital to multiple investors.

- providing our know-how and IP in market making available to this pooled capital.

Salient features of Delta’s AMM Pools:

- Single currency: pool comprises of only a single currency (BTC or USDT)

- One pool for multiple markets: Same pool can be used to make markets on multiple markets. For example – a BTC pool can theoretically make markets on all BTC settled contracts. This enhances capital efficiency.

- Leverage magnifies returns: The built-in leverage in derivatives magnify the trading gains of the market maker.

- Fixed capacity: an AMM pool only accepts capital that it can deploy profitably. Because of leverage, capital requirement is lower vs. spot market making.

- Enjoys latency advantage: The code of the AMM is co-located in the same virtual private cloud as our matching engine. Thus, the AMM pools enjoy almost an unfair advantage over external market makers.

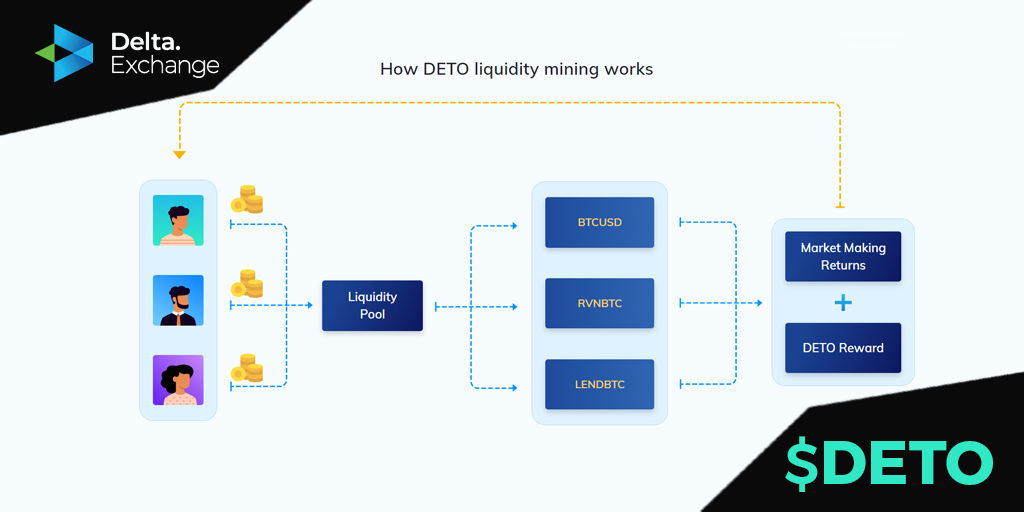

- Liquidity providers have three sources of revenues:

- (a) market making gains,

- (b) trading fee rebates from Delta and

- (c) DETO mined

[caption id="attachment_26983" align="aligncenter" width="800"]

DETO Liquidity Mining[/caption]

How does the AMM work

Our AMM is modeled after the market making firms in TradFi rather than the DeFi AMMs. The DeFi AMMs work quite well within the constraints imposed by being on-chain. Let’s take the example of the constant-product AMM of Uniswap. Using the constant-production pricing function completely removes the need for an oracle. Similarly, using the RFQ model eliminates the need for maintaining & updating multiple orders in an orderbook. While these design decisions have made bootstrapping liquidity for any pair really simple, they also have some downside. By not factoring in market conditions and price on other exchanges, the AMM results in liquidity providers leaving money on the table. This free alpha gets captured by arbitrageurs. Furthermore, the AMM uses capital quite inefficiently. Because the AMM chooses to show a price for any quantity, the available capital is spread over a wide range of prices. On a centralized exchange, where none of the blockchain related constraints are applicable, going with a simplistic AMM would be sub-optimal. Therefore, the AMM used by the pools run by Delta Exchange will instead do the following:

- Factors in information of a multitude of sources to decide its trading strategy

- Maintains and updates multiple buy and sell orders in the order book

- Allocates capital intelligently at different levels of the order book and across contracts

- Reacts/ predicts market conditions and tweaks its strategy accordingly. Can choose to show only bid, only offers or stay out of the market, reduce or increase leverage

- Has the intelligence to manage the risk of open positions

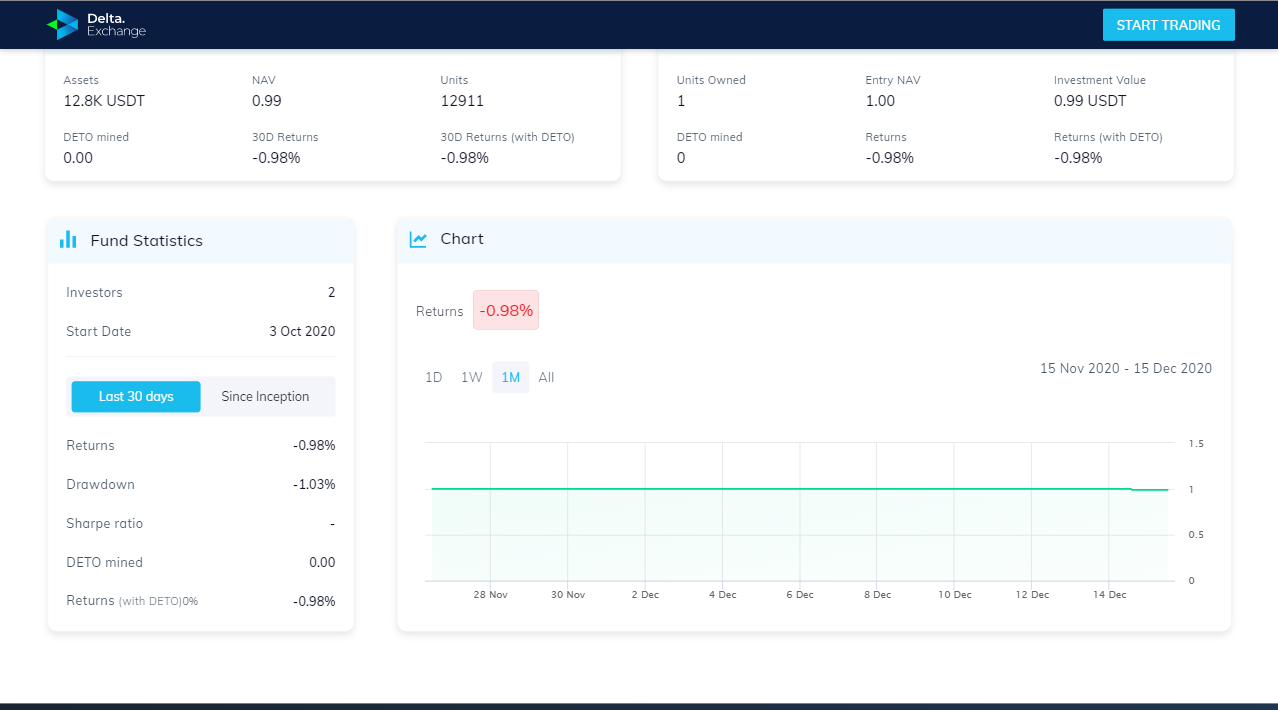

[caption id="attachment_26985" align="aligncenter" width="800"]

Fund Performance Dashboard (Beta)[/caption] The case for not making an AMM’s strategy public If an AMM is predictable, it is vulnerable to be front-run and taken advantage of. Smart traders and other market makers can anticipate the reaction of an AMM and position themselves to profit from the imminent action by the AMM. Consequently, liquidity providers loose out. Given this, we plan to disclose only the contours of the strategy that would be followed by our AMMs, but not their full code.

Future Directions

Initially, only the Delta Exchange team will have the privilege of creating and deploying an AMM. We however have no vested interest in keeping a tight rein on this. Over time, we will look to onboard more trading strategy creators (individuals or firms) and serve as a market place connecting capital providers with trading strategy creators. Secondly, there is no reason for us to restrict the AMM, rather the robo-trader, to only making markets. We plan to launch a wide variety (trend following, mean reverting, options seller) of robo-traders to provide liquidity providers varied and uncorrelated ways of generating returns on their capital.

For further updates on the launch of liquidity mining and DETO; please join Delta's Telegram group here.

Frequently Asked Questions (FAQ)

Q1: What are Delta Exchange’s AMM Pools and how do they work?

Answer: Delta Exchange AMM Pools let liquidity providers deposit capital that gets automatically used to quote both sides of derivatives markets. Returns come from trading fees, spreads, and funding rates, with no active position management needed from the LP side.

Q2: What are the key features and benefits of Delta's AMM Pools for liquidity providers?

Answer: LPs get passive exposure to market-making returns without running individual positions. Capital is deployed automatically across multiple assets, with leverage available to scale up fee income. The strategy handles quoting, rebalancing, and risk controls without any manual input required.

Q3: How does leverage enhance returns for liquidity providers in Delta's AMM Pools?

Answer: Leverage lets the pool deploy more notional capital than the raw deposit, scaling fee and spread income proportionally. The tradeoff is that losses scale the same way. LPs should understand this clearly before opting into higher leverage tiers.

Q4: What are the three sources of revenue available to liquidity providers in Delta's AMM Pools?

Answer: LPs earn from taker fees on each trade, bid-ask spreads as the pool quotes both sides of the market, and funding rate payments when the pool carries directional exposure. The revenue mix shifts with volume and market conditions.

Q5: Why does Delta Exchange keep its AMM strategy private and not publicly disclose it?

Answer: Publishing the quoting algorithm would let competitors and informed traders front-run or exploit it systematically, which would hurt LP returns over time. Keeping it private protects the edge that makes the pools competitive against fully transparent on-chain AMMs.

Q6: What are the plans for Delta's AMM Pools and Robo-trading strategies?

Answer: Delta Exchange has expanded its AMM pool offerings since launch, adding Robo-trading strategies across different risk profiles. The platform's direction has been to give retail and institutional LPs more control over their exposure without requiring active trading on their part.