Digital Derivatives – Scaling DeFi From Billions to Trillions

DeFi is currently the most exciting part of the crypto ecosystem and is buzzing with activity. Despite the explosive growth on the back of Compound’s liquidity mining in the last one month, DeFi money markets are currently tiny. According to Loanscan.io, the total pending loans today are slightly north of $1 billion. In comparison, a single centralised platform like Genesis Capital had over $650 million in active loans as of Q1 2020. In this article, we focus on DeFi money markets, explain the constraints that currently are a drag on their growth and envisage a path to take DeFi lending from billions to trillions of dollars.

Growth Constraints for DeFi Money Markets

Limitations from Collateral

Currently, there are three defining characteristics of DeFi lending:

(a) all the loans are collateralised

(b) only those crypto-assets that are present on the Ethereum blockchain can be used as collateral

(c) the loans are heavily collateralised, with collateralisation ratios typically ranging from 1.5-3x.

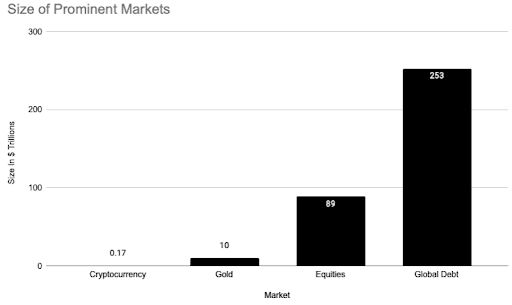

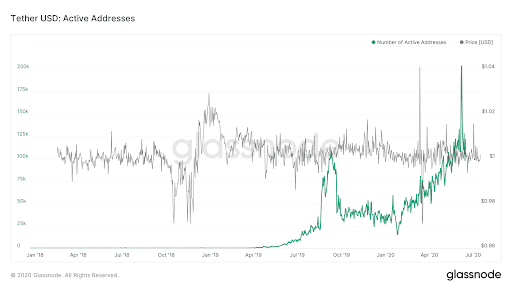

Considering how early we are in the evolution of DeFi lending, all these make sense. Having loans secured by collateral is the easiest way to make lending trustless and free from intermediaries like banks. However, this also puts a natural limit on how big DeFi lending can become. The maximum amount that can be lent out is capped by value of available collateral. The market-cap of Ethereum limited the amount of loans in DeFi for quite some time. Assuming 10% of Ethereum’s market-cap was active in DeFi, that figure will be around ~$2.5 billion. If a 1.5x collateral requirement was made then the upper limit for loans issued with Ethereum backing will be at around $1.66 billion. This challenge was already detected by the Ethereum community early on and several ERC-20 tokens were made acceptable as collateral on platforms like Maker, Compound and Aave. Another way this expansion happened was with the movement of USDT to the ERC-20 standard. In the past few months, as liquidity mining on Compound increased substantially, we saw how USDT supply ballooned to enable investors to exploit that opportunity. This has also aligned with a major rise in the number of active user addresses on Tether.

As things stand today, the total combined market cap of Ether and ERC-20 tokens is $50+ billion. So, that’s the value of all available collateral for loans.

Looking Beyond Lending For Usage

Speculation is the key utility of multiple digital assets today. This is true for DeFi money markets too. Margin trading seems to be the driver of almost all the borrowings. For DeFi to reach its potential and be an alternative to traditional finance, it has to be able to cater to all various other much larger use cases for loans. For individuals, this includes mortgages, vehicles loans, personal loans etc. And, for companies, this includes working capital loans as well as longer-term borrowing to finance capex and growth.

Anecdotal evidence suggests that some of this has started to happen recently. The allure of yield farming has prompted bitcoin miners to shift to DeFi platforms for managing their working capital. These miners were earlier using companies like Genesis to get USD loans by keeping their bitcoin as collateral. So, Genesis is replaced by DeFi platforms like Compound and Aave and USD loans are replaced by USDC/ USDT loans. These are very early days and it remains to be seen if this trend will sustain.

Growing from Billions to Trillions

The hurdles in DeFi’s path to scale are certainly formidable, but not insurmountable. We expect most of these roadblocks will be addressed as the crypto ecosystem matures, increasing smart contract adoption and innovation in crypto-native business mode.. In the rest of the article, we highlight some of the key possible milestones in the likely billion-to-trillions path of DeFi money markets.

1. Expansion of the Digital Assets Universe Accessible to DeFi

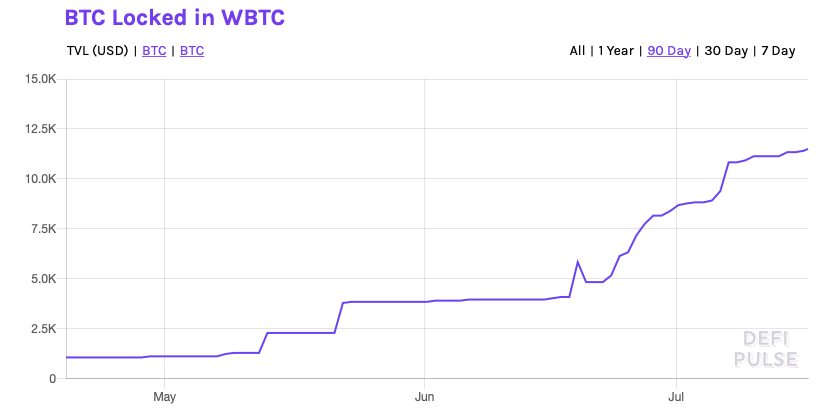

MakerDAO started with a single collateral DAI (only Etherereum), but moved to multi-collateral DAI in late 2019. Now, USDC, TUSD, WBTC, KNC, ZRX and BAT are also accepted as collateral to borrow DAI. Similarly, Compound and Aave have been expanding the number of assets they enable. Our understanding is that the initial wave of collateral expansion in DeFi will come from providing a variety of the number of tokens that are accepted. This will allow users with different tokens to take loans without losing exposure to the underlying asset itself. The target-group for this base is power users in DeFi who already own a wide variety of digital assets. One way we saw this transition happening already is with the rise of ERC-20 USDT. More importantly, Bitcoin has also been moving to Ethereum blockchain in the form of Wrapped Bitcoin. Stablecoins and wrapped assets represent a conduit through which assets and consequently value accumulates in the Ethereum ecosystem. The more this happens, the more the opportunity size for DeFi increases.

Finally, as the market-cap of assets within the digital asset space increases - the amount that can be loaned will also increase. This is entirely reliant on the price appreciating in the future.

2. Market Expansion Through Credit Delegation

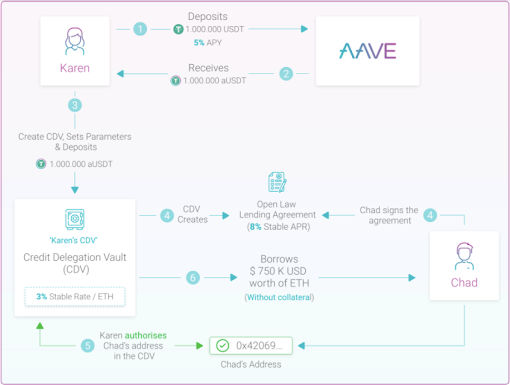

Credit Delegation is a new feature on the Aave Protocol which enables money lenders to make uncollateralised loans. The lender supplies money to the Aave Protocol, but is able to earn a premium for assuming additional risk of default. The default risk of these unsecured loans needs to be managed by the lender off the protocol.

As of now credit delegation cannot happen in a trustless manner, and this facility is likely to be used by businesses that already have a level of trust with each other. However, over time, new protocols can be built on top of the Aave Protocol to facilitate underwriting of unsecured loans. This could happen in the form of credits scores or through collateralisation of future cash flows. We discuss these below.

3. Access to Physical World Assets Through Tokenisation

As the market for digital currency based collateral saturates, platforms will need to consider traditional instruments to expand into. The closest associated markets today are commodities and traditional securities. One way this could happen is through creation of synthetic instruments on platforms like UMA Protocol or Synthetix. They allow individuals to take exposure to gold without owning the physical asset itself. The other way this could occur is from centralised alternatives such as Paxos gold that offer a digital representation of a commodity as a token. It can then be used as a deposit for a loan. By expanding to commodities and securities as collateral types, blockchain based lending will be able to add another $20 trillion to the cap of how much can be loaned out. Since commodities like Gold have lower volatility, they could prove to be better lending instruments through lower collateral requirements. We will also see the tokenisation of real-life assets such as real estate, art and even intellectual property rights in the future.

4. Rise of Blockchain Native Businesses

As the crypto ecosystem matures, beyond speculation, many more use-cases for DeFi lending will become practical. One way this will play out is as income share agreements (at the individual level) and cash-flow based lending for businesses that function primarily on-chain. Businesses that use only stable-coins as a payments mechanism can have their credit-worthiness easily assessed by handing over their wallet addresses. Bonds could be issued by startups to give individuals rights to their future cash-flow. This could be an alternative to equity based financing and create an alternative exit route for venture. Startups like Centrifuge.io are already working on making cash-flow tokenisable. A third party could then explore how their income and expenses balance. This data could be used to create a credit score on the basis of which investors could offer loans. For blockchain-first businesses that work with remote employees, this means being able to empower employees to have access to financial services that may otherwise not be available. A DAO for instance could be used to give out loans in a cooperative model with a part of the future income going towards loan repayment.

5. Data Driven Credit Scores

As the hunt for yield in DeFi grows with more traditional funds coming into the ecosystem we will likely see a blockchain based network being used for lending in different parts of the world. They will disintermediate banks and offer loans directly on basis of identity and credit-scores. In these instances, the advantage for institutions will be the cost benefit of not requiring a physical infrastructure and sourcing liquidity from individuals around the world to disperse loans to. This will have a high degree of risk in terms of repayment collection as there may be no collateral. However, it is likely that traditional lending markets and blockchain based lending collude in this fashion. The end user will barely know a blockchain was used for processing their loan application and making the necessary credit line available. It is inevitable that blockchain based lending grows far beyond the existing collateral types. The primary challenge with DeFi today is that it is accessible only to those that use digital assets and the key use-case is trading. As the collateral types in DeFi expand, the lines between CeFi and DeFi will blur and it will become a natural evolution of fintech as a whole. Blockchains will become the infrastructure layer on which financial transactions are settled at a global scale. More importantly with increasingly digital assets such as future cash-flow of a self-driving car or NFTs that represent in-game assets. The next decade will have a lot to look forward to in the lending space. The key difference we will be seeing will be in terms of expansion of the variety of assets that are used for lending and the speed at which loans are offered. More importantly, lending will become a more global activity much like how Stripe and Paypal initiated global payments.

About the Authors

Joel John: is a research analyst specialising in blockchain related investments. You can follow him on Twitter or subscribe to his Substack

Jitender Tokas: is the Co-founder and Chief Business Officer of Delta Exchange. Prior to starting up, Jitender was a stock analyst with Citi and has over a decade of experience in financial markets. You can follow him on Twitter.

Frequently Asked Questions (FAQs)

Q1: What limits DeFi money market growth?

Answer: Over-collateralization is the main bottleneck. DeFi borrowers must lock more value than they borrow, typically 150% or more, which shuts out anyone without excess crypto holdings. Without on-chain identity infrastructure, undercollateralized lending stays mostly unsolved.

Q2: How does collateral restrict DeFi lending?

Answer: Only capital-rich participants can borrow meaningful amounts, since every loan requires collateral worth more than the loan itself. Falling collateral values trigger liquidation cascades that amplify price drops. On Delta Exchange, derivatives traders often position around these volatility events.

Q3: What is credit delegation in Aave?

Answer: Credit delegation lets Aave depositors extend unused borrowing capacity to trusted third parties without moving funds. The delegatee can borrow uncollateralized up to the limit. Aave V3 added finer controls, but adoption stays low given the counterparty trust required.

Q4: How can tokenization expand DeFi lending?

Answer: Tokenizing real-world assets like US Treasuries, real estate, and trade invoices lets them serve as on-chain collateral, expanding the base beyond crypto-native assets. BlackRock's BUIDL and Franklin Templeton's FOBXX have tokenized billions in Treasuries now actively used in DeFi.

Q5: What are blockchain-native credit scores?

Answer: Blockchain-native credit scores use on-chain data like repayment history, wallet age, and protocol activity to assess creditworthiness without traditional identity. Spectral Finance explored this approach. Sybil resistance, preventing one person from running multiple clean wallets, remains the main unsolved barrier.

Q6: How does Wrapped Bitcoin help DeFi?

Answer: Wrapped Bitcoin (WBTC) is an ERC-20 token backed 1:1 by BTC in custody, letting Bitcoin liquidity enter Ethereum-based DeFi as collateral. In 2024, BitGo transferred custody to a Justin Sun-linked entity, raising trust concerns and spurring Coinbase's cbBTC launch.

Q7: Can DeFi replace traditional banking?

Answer: DeFi replicates lending, borrowing, and yield functions but cannot replace banking at scale. Undercollateralized credit and poor UX are the real blockers. MiCA, in force since December 2024, is pushing regulatory clarity. Delta Exchange offers DeFi token access via derivatives.