Digital Derivatives – CBDCs: Looking Beyond The Hype

The internet has given a huge boost to digital currencies, and cryptocurrencies have been at the vanguard of this trend. In a short period of time, Bitcoin and other cryptocurrencies have had a significant impact on the world, catalyzing central banks around the world to come up with their own digital currencies. In this article, we do a deep dive into Central Bank Digital Currencies - understanding their design, the current stage of evolution and their potential impact on peer-to-peer cryptocurrencies like Bitcoin.

What are CBDCs?

CBDCs are fiat-money issued by a central bank in digital form. A CBDC can be implemented using a database run by the central bank in collaboration with approved private sector entities. Blockchain technology is not necessary for issuing CBDC; however, a central bank can possibly run a private blockchain with a consortium of banks to implement CBDC.

Potential Benefits of CBDCs

CBDCs can go a long way in modernizing payments and value transfers in a digital economy, holding the potential to radically alter the way individuals and organizations transact. They possess a range of unique characteristics and bring a host of benefits to consumers, including:

- Faster transactions that require less documentation and time to settle, resulting in lowered costs for sending and storing capital whilst enabling faster trade across regions.

- More efficient cross-border transactions.

- More efficient distribution of resources e.g. emergency stimulus cheques.

- Creation of stronger links between identity and payments.

- Prevention of money laundering and terrorist financing due to better tracking and monitoring of financial flows.

We do however note that some of the benefits of CBDCs will come at the expense of privacy and anonymity. This may drive people towards P2P cryptocurrencies.

CBDCs vs. P2P Cryptocurrencies

Cryptocurrencies to date have been issued by non-governmental entities as non-legal tender, as exemplified by Bitcoin. CBDCs add a novel spin to this, existing as a legal tender issued by a central bank. Both CBDCs and cryptocurrencies exist in a purely digital format - with no physical complement - allowing for instantaneous transactions and seamless transfer across geographical regions. That said, there are a number of key differences between the two types of digital currency:

| CBDCs | P2P Cryptocurrencies |

| Centralised system of control | Decentralised system of control |

| Technology-neutral | Blockchain/DLT-based |

| KYC-enforced | Pseudonymous (anonymous in extreme cases) |

| Concentrated control and interference | Resistant to censorship and interference |

| Monetary policy: adjustable, centrally-driven and opaque | Monetary policy: Pre-defined, algorithmically-driven and transparent |

| Credit-asset; Intended as a legal tender | Commodity-asset; Not recognised as legal tender |

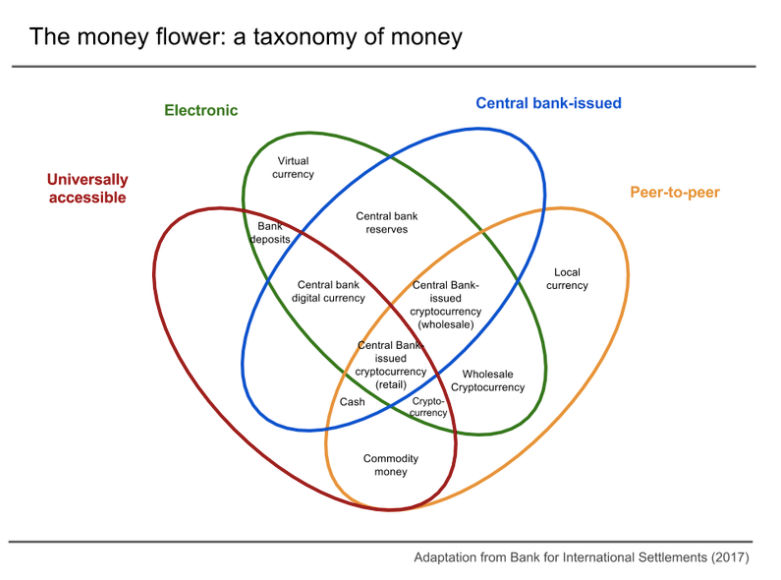

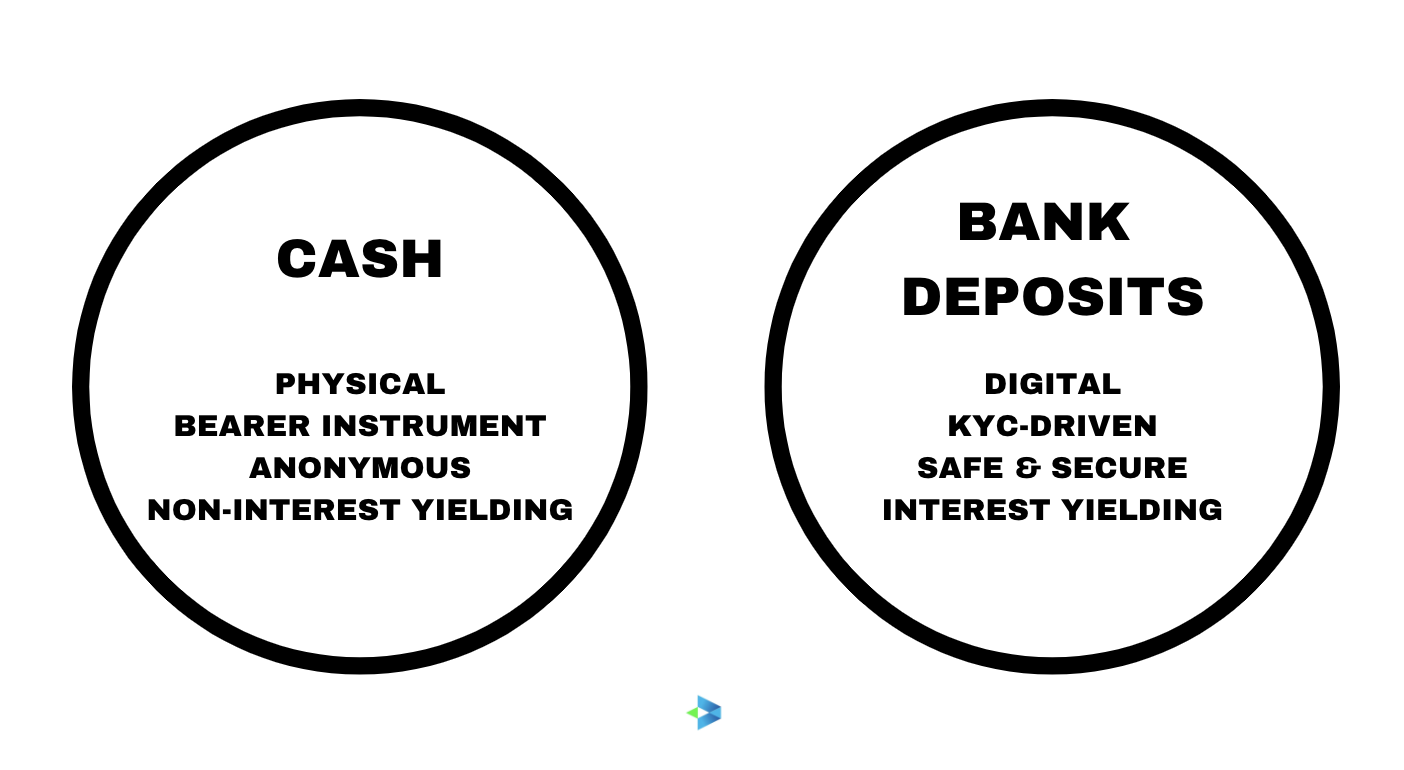

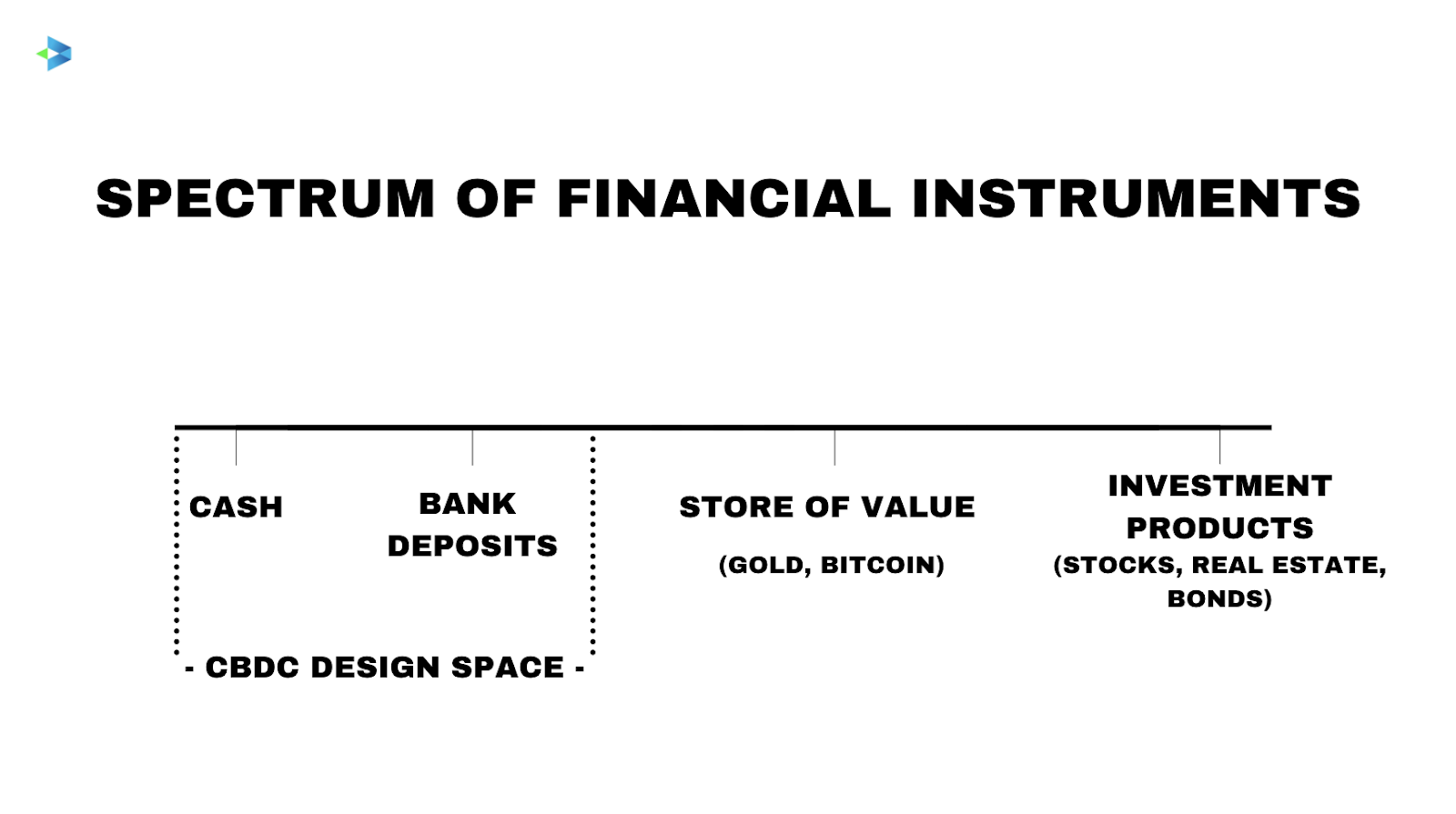

The CBDC Design Space: Cash vs. Deposit Spectrum

CBDCs are a digital version of central bank liability (cash in the economy & commercial bank reserves). They can combine the digital aspects of bank deposits with P2P transactional anonymity of cash. In fact, the design space of CBDCs lies between cash and bank deposits.

The beauty of CBDCs is that they can combine the characteristics of both cash and bank deposits to create novel payment & store-of-value instruments.

- A cash-like CBDC: Such a CBDC will essentially be digital tokens (think digital representations of currency notes) that can be exchanged for goods and services. Like cash, these tokens will be bearer instruments with full anonymity. A cash-like CBDC can potentially replace physical cash.

- A bank deposit-like CBDC: Such a CBDC will represent an account opened with a central bank. It may have all the features of a digitized bank deposit. The key difference from status-quo here is that retail people will be directly able to open accounts with the central bank. Currently, only commercial banks have this privilege. Such a CBDC can lead to disintermediation of banks. If banks are unable to raise deposits, they won’t be able to make loans, contributing to a knock-on effect on the credit supply in the economy. On the flip side, the disintermediation of banks will increase the central banks influence over money supply and the economy .

A CBDC design will entail trade-offs between the characteristics of cash and bank deposits, depending upon the objectives of a central bank. A good example of such a trade-off is anonymity. Cash is fully anonymous and bank deposits are fully KYC’ed. However, a CBDC can provide varying levels of anonymity:

- Partial Anonymity: Anonymity towards the public and other third-parties, but no anonymity towards the authorities.

- Transactional Anonymity: Anonymity below certain transaction amounts (as implemented by a number of digital asset exchanges).

- Conditional Anonymity: Full or partial anonymity potentially lifted through government intervention (e.g. a court order).

Similarly, interest rate is another lever a central bank can play with. If it wants the CBDC to be a cash alternative, but still wants to preserve physical cash, the central bank can set negative interest rates on the CBDC. CBDCs are valuable due to their ability to blend the benefits of cash and bank deposits, creating a novel payment/ store-of-value instrument in the process. An instrument which seamlessly blends the privacy benefits of cash with the security and interest-bearing benefits of digital deposits would go a long way in a modern society. We believe that CBDCs are likely to be closer to cash than to bank deposits. This is because the implications on banks from a CBDC that’s closer to bank deposits can be quite serious. Banks play an important role in credit flow and hence, economic growth. That said, even a cash-like CBDC will have certain features of bank deposits - such as interest - and some level of identity verification.

The Current State of CBDCs

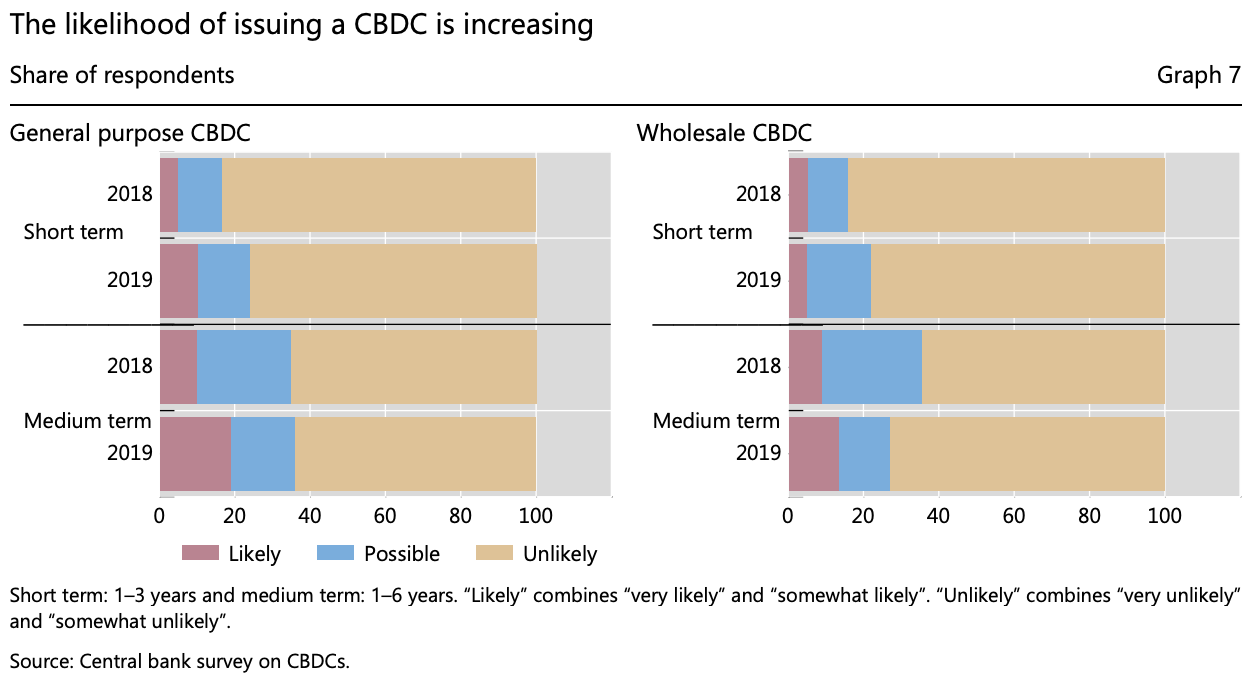

Several central banks in both advanced and emerging economies are currently working on the design and implementation of CBDCs, including Australia, Brazil, China, Denmark and Philippines.

According to a January 2020 study by Bank for International Settlement (BIS) has shown that over 80% of analysed advanced economies are actively conducting work on the development of CBDCs. This includes the Fed, ECB, BoE and BoJ. Adding to this, nearly 40% of central banks consider it likely or possible that a general purpose CBDC will be issued in the medium-term.

As of now, only Sweden and China seem to be seriously considering the launch of a CBDC. For Sweden the catalyst is the diminishing use of cash in its economy. In China, the central bank (PBoC) is looking to retain control in the face of rise in retail digital payments facilitated by Big Tech companies. China is furthest along in the implementation of a CBDC; however, the question of what form a digital RMB will take is currently uncertain. Adding to this, China will probably attempt to break the dollar hegemony by promoting adoption of digital RMB as the currency for international trade.

The Relationship Between CBDCs & Stablecoins

Stablecoins are blockchain-based digital currencies which possess the dual benefits of blockchain digitalisation and stability of fiat currencies. Stablecoins are typically pegged to fiat currencies, although now we have commodity backed stablecoins too.

The peg to fiat currencies is maintained through one of the following methods:

(a) fiat-collateralisation,

(b) crypto-collateralization

(c) algorithmic supply management.

Among these, fiat-collateralised stablecoins, like USDT, currently dominate the space. In May 2020, the total aggregate supply of stablecoins surpassed $11 billion, from $4 billion in June 2019, as a testament to the growing popularity of these assets. Fiat-collateralized stablecoins in many aspects are quite similar to CBDCs. Stablecoins have (and CBDCs can) made (make) the transfer of funds between two parties across different locations cheap, efficient, and transparent. In contrast, traditional cross-border payments are slow, expensive and exceptionally opaque. Central banks are likely to exert tight control over CBDCs. Their management of CBDCs (interest rates, supply etc) will be driven by the central banks’ macroeconomic objectives. In contrast, stablecoins are purely supply-demand driven and are widely accessible to people around the world. They also represent a highly flexible and accessible alternative to a USD bank account for traders around the world for whom this may be extremely difficult to obtain.

We believe that the market-driven nature of stablecoins provides them a significant edge over CBDCs. However, since stablecoins are going to compete head-on with CBDCs, central banks may feel threatened by them and make it difficult to issue stablecoins. An unrelated but interesting aspect of stablecoins is the facilitation of a societal shift from credit money to commodity money through the adoption of commodity-collateralised stablecoins. While central banks and credit money is based around a system of liabilities, commodity money, like gold, doesn’t serve a monetary function. Commodity-collateralised stablecoins can change that and lead to the revival of commodity money.

CBDCs vs. Libra

In May 2019 Facebook announced plans for Libra - a stablecoin tied to a basket of national fiat currencies, built in conjunction with Shopify, Uber, Coinbase and many more. While the stated primary function of Libra is global remittances, its use-cases are quite likely to overlap with cash. The announcement of Libra prompted central banks to pay close attention to this field, likely due to the scale of the Libra proposal and its primary backer, Facebook. With more than 2.5 billion users, the Facebook ecosystem can be thought of as the world’s largest ‘digital nation’. Libra has the potential to function as an easily-obtainable payment instrument for the many millions of unbanked. If Libra becomes the currency which powers transactions (both P2P and B2C) in this ecosystem, then it can potentially leave many fiat currencies irrelevant. Widespread adoption of Libra could weaken the hold central banks have on the respective money supplies in their countries and weaken the influence of monetary policy actions. Thus, governments and central banks around the world see Libra as a potential threat to sovereign currencies, including CBDCs. That’s the reason there have been calls to tightly regulate Libra - or outright ban it.

CBDCs Impact on Bitcoin

We believe CBDCs will have little to no direct impact on Bitcoin. Bitcoin functions as digital gold, where CBDCs are the cash and savings deposit equivalent. They are unrelated instruments, with different purposes and functionalities, and the impact of one on the other should be largely neutral.

Whilst there is little direct impact, positivity surrounding CBDCs highlights the second-order benefits to assets like Bitcoin. The public reception to Libra, whilst not a pure CBDC, highlights the impact of large-scale digital asset adoption - through a nation or a corporation - and how the launch of a CBDC drives excitement in the education and adoption of Bitcoin.

A vital driver in the adoption of Bitcoin is its underlying emphasis on independence, which no CBDC will be able to effectively replicate. For this reason, a CBDC is unlikely to ever impact the adoption of Bitcoin negatively. On the contrary, the educational benefits a CBDC would bring to space would transfer over to Bitcoin, building upon the existing mainstream growth of these assets. In the future, the rise in CBDCs may work to cement the anonymity-focused benefits of Bitcoin, further growing the popularity of Bitcoin. Bitcoin as an asset functions as a highly-accessible, pseudonymous, decentralized, and non-sovereign version of a CBDCs, and it may be the case that the unique benefits of this remain unclear to users until after the effective implementation of CBDCs.

Frequently Asked Questions (FAQ)

Q1: What are CBDCs?

Answer: CBDCs are government-issued digital currencies, distinct from cash, bank deposits, or private stablecoins. Over 130 countries are in some stage of development or deployment as of 2025, including China's e-CNY, India's e-Rupee, and the EU's ongoing digital euro pilot.

Q2: How do CBDCs differ from cryptocurrencies?

Answer: CBDCs are centrally issued with full government control, transaction surveillance, and programmable restrictions. Bitcoin is decentralized, censorship-resistant, and capped at 21 million coins. Traders on Delta Exchange often treat BTC as a direct hedge against this kind of monetary control.

Q3: What is a cash-like CBDC?

Answer: A retail CBDC is designed for everyday public use, held directly without a bank intermediary. China's e-CNY is the most deployed example, with hundreds of millions of registered wallets and active use in domestic commerce and government payments.

Q4: How do stablecoins relate to CBDCs?

Answer: Both aim to provide stable digital value but differ fundamentally in who issues them. MiCA, in force since December 2024, requires strict reserves from stablecoin issuers. CBDC rollouts could squeeze private alternatives like USDT and USDC over time.

Q5: Which countries are developing CBDCs?

Answer: China leads with e-CNY in active domestic use. India's e-Rupee pilots continue. The EU digital euro is in its pilot phase. In January 2025, President Trump signed an executive order explicitly prohibiting development of a US retail CBDC.

Q6: What is Libra and why is it controversial?

Answer: Libra was Meta's proposed global stablecoin, later renamed Diem. Regulators worldwide objected over monetary sovereignty and financial crime risks, and Meta shut it down in January 2022. It has been referenced in almost every major stablecoin policy debate since.

Q7: Will CBDCs negatively impact Bitcoin?

Answer: Most evidence suggests CBDCs strengthen Bitcoin's appeal. Normalizing digital money while demonstrating government surveillance risk reinforces exactly what BTC offers. Spot ETF inflows since January 2024 confirm institutional interest. Traders can access BTC on Delta Exchange with INR settlement.