Markets

Futures

Options

Delta Exchange Blog

Delta News

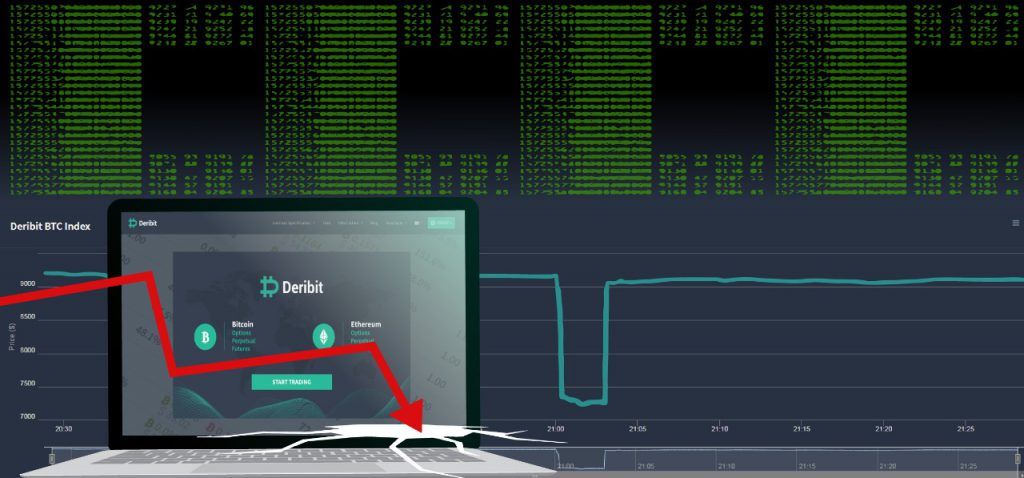

Decoding DeriBit’s Flash Crash on Halloween

Delta Exchange

November 4, 2019

Share