Bitcoin Price Seasonality: Long in November & Short in January

Price seasonality refers to recurring fluctuations in price during particular periods of the year. Over the years, this results in formation of an easily identifiable pattern or style. Seasonality is found in the prices of a range of assets such as currency, equity, and even derivatives. In traditional financial markets, these seasonality patterns are well known and get priced in almost completely. Cryptocurrency markets are not as efficient as traditional financial markets. Thus, identifying seasonal patterns might lead to profitable trades. Since bitcoin is the cryptocurrency with the longest history, in this article we will analyse Bitcoin prices and look for seasonality.

Seasonal Patterns in Stock Markets

Stock markets have a bunch of very well established seasonal patterns. These patterns have catchy names like ‘Sell in May and go away’, January Effect and the ‘Santa Claus Rally’, which help catch the attention of traders. Plenty of research papers have tried to understand the reasoning behind price seasonality with a major portion of the conclusion driving it to reasons related to human behaviour and sentiment. Once a pattern is known and predictable, traders will start positioning for the anticipated price moves. This in turn would make the seasonal pattern weaker. This is exactly what we have seen play out in US stock markets. The price seasonality used to be stronger in the past periods compared to recent trends. This is a sign of increasing market efficiency.

Price Seasonality in Bitcoin

Relative to stock markets where decades of prices are available, bitcoin has very limited price history available. Still it is worth looking for seasonality in Bitcoin because cryptocurrency markets are a lot less efficient compared to stock markets. Thus, any seasonal patterns in Bitcoin can potentially be exploited for making profitable trades. Instead of mining Bitcoin price data to seek patterns, we felt a better approach was to check if the seasonal effects that are visible in stock market are also present in Bitcoin. Additionally, we looked at quarterly and half-yearly price performance of Bitcoin. We summarize the insights from this work below.

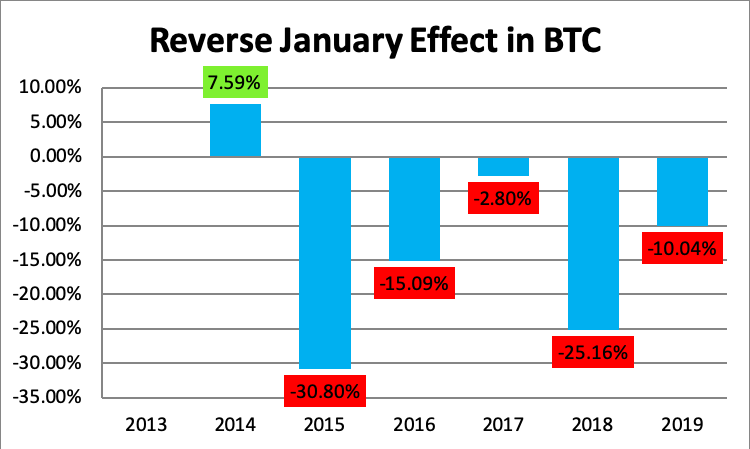

January Effect

The U.S. Equity Stock Markets monitor a price seasonality during the month of January. It has been observed that during this month the prices have surged abnormally high due to the New Year and Holiday Effect. This trend is known as the January Effect. However, while analysing the bitcoin price movement, there has been a ‘Reverse January Effect’ that has been observed. Out of the 6 years, only 2014 have shown a bull run, while the rest of the years have had a negative price return.

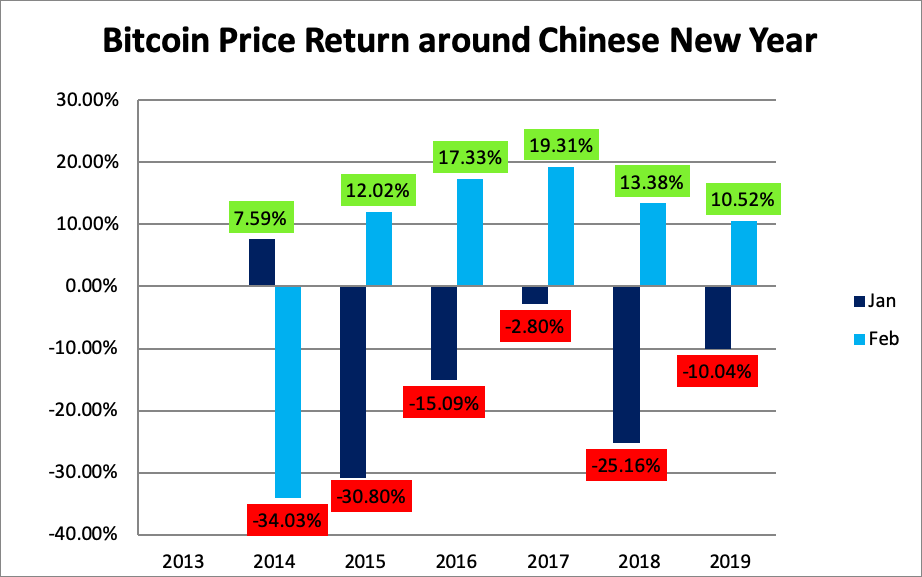

Chinese New Year Effect

Another price trend that is seen in Bitcoins is the Chinese New Year effect. Since Chinese investors are big holders of bitcoin, their collective actions can have a material impact on bitcoin’s price. Around Chinese New Year bitcoin price tends to be under pressure as investor’s cash-out from bitcoin to fund their expenses. This dip is usually seen 4-6 weeks before the Chinese New Year which is in the month of January and could be one of the reasons for the ‘Reverse January Effect’. Post the Chinese New Year there has been a gradual increase in the price which has been observed in all the months of February from 2015 to 2019. Only the year of 2014 has had a negative monthly price return.

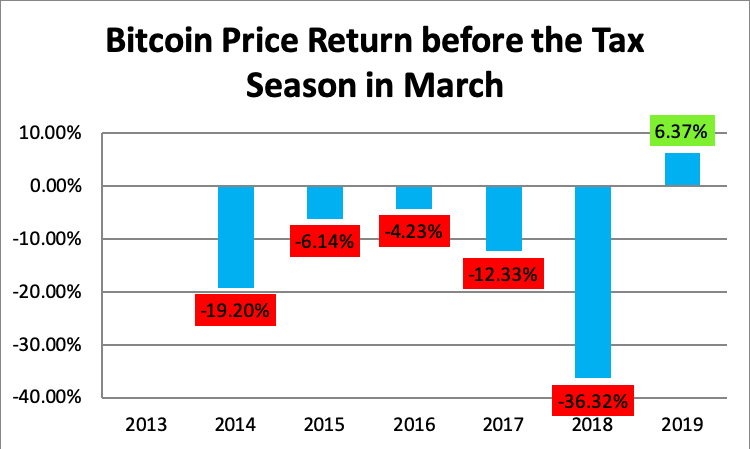

Tax Effect

An additional price trend that can be seen is the March tax effect, where many investors cash in their bitcoins to pay their U.S. Annual Taxes. Since 2014, all the months of March have had a negative monthly return except for the year of 2019 where the monthly gain was 6.37%. This sell-off is observed in the U.S. Equity market also and hence, the month of March could be correlated in both these sectors.

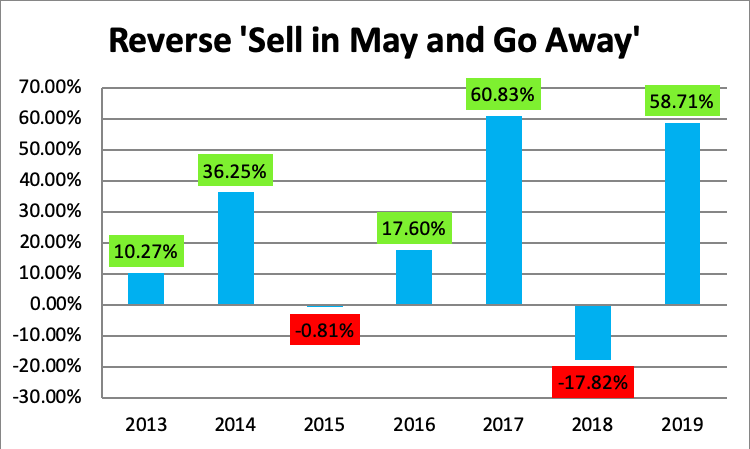

Sell in May and Go Away

The month of May usually sees a dip in the U.S. equities as investors and traders prefer closing their positions before the start of the summer holidays. The ‘Sell in May and Go Away’ price trend has also worked in the reverse trend while we’re talking about bitcoin. Through the years of 2013 to 2019, 2015 and 2018 have only been the two years to have a negative monthly return whilst the others have shown at least a 10% gain in May. The highest May return was the year 2017 with a whopping 60.83% return.

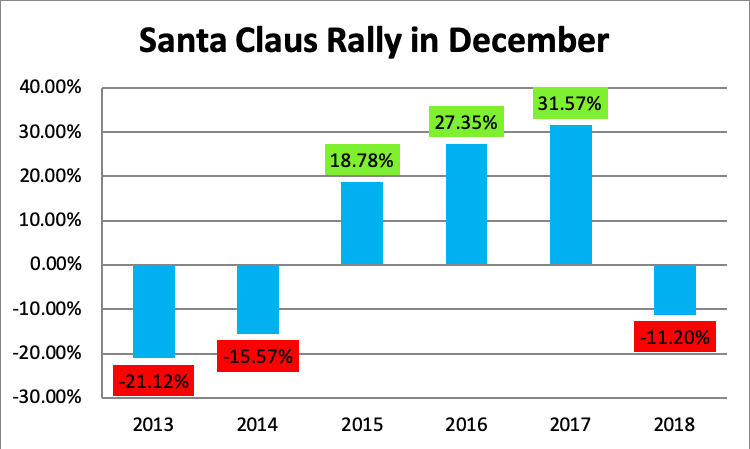

Santa Claus Rally

While the ‘Santa Claus’ rally has shown positive monthly returns in the U.S. equity segment, while analysing the data for BTC’s in particular, the conclusion has been mixed. Though only 6 years of data is present for the research, the years of 2015,2016 and 2017 have given positive monthly returns whilst the remaining have been negative. However, when taken all the year's returns on average, the December monthly returns have been positive by a mere 5%.

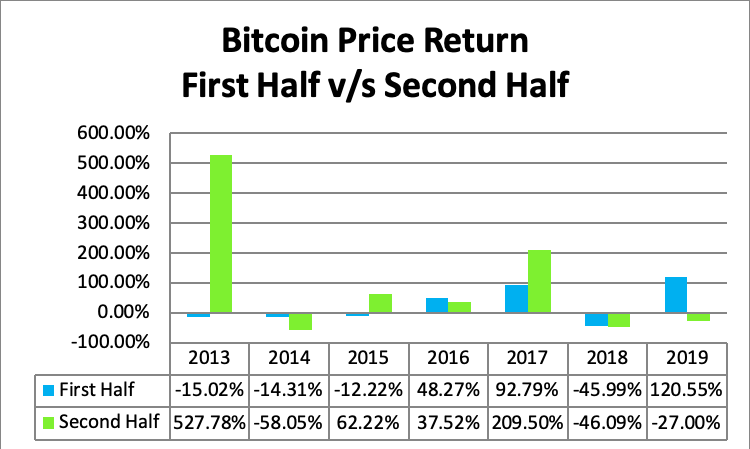

First Half vs. Second Half

An important trend that is observed in the cryptocurrency world and especially Bitcoins is the Bull Run in the second half of the year as compared to the first half. Back-testing research has anyway shown the last quarter is more profitable compared to the earlier quarters. Along with this, the second half of the year is more profitable compared to the first half.

When to long Bitcoin and when to short it

From all the discussions we have had above, another trend has come to light. Through past research, numbers have shown Q1 has on an average been negative while a major chunk of the gains can be attributed to Q4. This could co-relate with ‘Reverse January Effect’, ‘Tax Season’ and ‘Santa Clause Rally’. With this analysis, one can draw a conclusion to dump in Q1 and hodl in Q4.

| Q1 | Q2 | Q3 | Q4 | |

| 2013 | -15.02% | 46.77% | 481.01% | |

| 2014 | -45.65% | 31.34% | -46.73% | -11.32% |

| 2015 | -24.92% | 12.69% | -4.76% | 66.98% |

| 2016 | -1.99% | 50.27% | -6.17% | 43.70% |

| 2017 | 4.18% | 88.61% | 79.82% | 129.68% |

| 2018 | -48.10% | 2.11% | 6.24% | -52.34% |

| 2019 | 6.85% | 113.70% | -27.10% | |

| AVG | -18.27% | 40.53% | 6.87% | 109.62% |

Final Thoughts

While price seasonality should not be used as a price prediction model, there are a few months where the trends can be used alongside other research methodology to make an investment or trading decisions. Even with the limited data that is present, there are few trends such as the ‘Reverse January Effect’ or the ‘Santa Claus Rally’ which have shown reasonable seasonality. However, we need longer price history to reach stronger conclusions.

Source: BTC Price - https://coinmarketcap.com/currencies/bitcoin/historical-data/?start=20130428&end=20191104